In the heart of Southern Africa, Malawi’s banking sector has long been a source of frustration for its customers. From endless queues at branches to unreliable digital services. Frequent network outages in the rural areas, declined debit cards for customers temporarily outside Malawi, and crippling foreign exchange (forex) shortages, the complaints are relentless.

Social media platforms like X (formerly Twitter) and online forums overflow with stories of poor customer service, malfunctioning cards, and a pervasive sense of institutional incompetence that leaves account holders feeling more like burdens than valued clients.

The Forex Fiasco

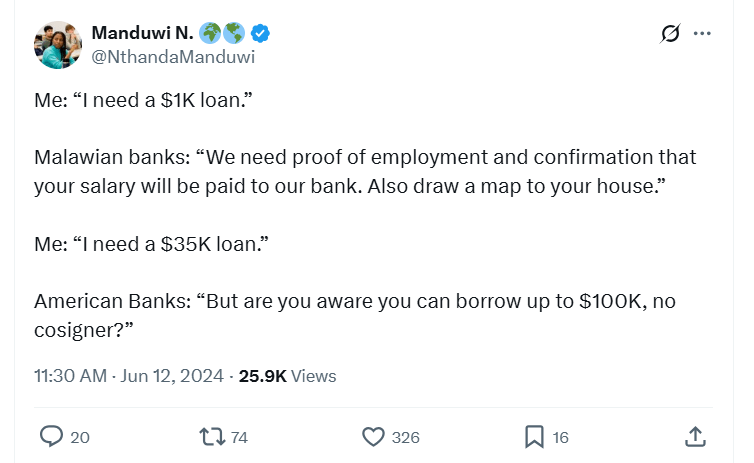

One of the most glaring problems in Malawi’s banking system stems from the country’s chronic forex shortages. Malawi, being landlocked and heavily reliant on imports, has over the last few years faced dwindling foreign currency reserves, leading recently to strict controls on forex access. This has directly impacted everyday banking, and business transactions particularly for those needing to make international transactions or use cards abroad.

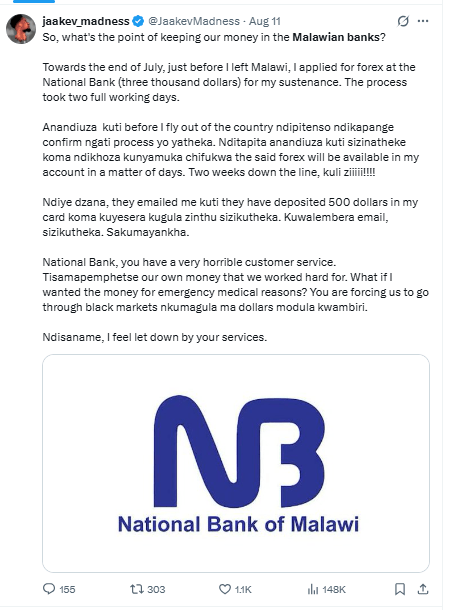

Customers routinely report applying for forex only to face bureaucratic delays stretching for days or weeks. A Facebook user, Blessings Chikapa, shared his frustration with National Bank of Malawi, stating, “I applied for $3,000 in forex and was told it would take a few days. Two weeks later, nothing had materialized, and I was forced to use expensive black market options.” Similar stories abound of students unable to pay tuition fees abroad, businesses missing critical payment deadlines for imported goods, and travelers stranded without access to funds for international trips.

Institutional incompetence compounds these challenges. While the Reserve Bank of Malawi (RBM) issues reports challenging the industry to improve forex management, customers bear the brunt of internal failures. The auction systems for forex allocation have been derided as “a terrible joke,” with stark mismatches between official rates and black-market realities leaving people unable to access funds for essentials like medical emergencies or educational expenses.

Some customers report being denied forex altogether despite meeting official requirements, only to discover the same currency available through informal channels at significantly inflated rates.

Customer Service Nightmares

Malawian Banks don’t know the meaning of customer service. Period. Because beyond the forex woes, poor customer service remains a recurring theme in critiques of Malawian banks. The Consumers Association of Malawi (CAMA) has publicly criticized banks for inadequate service delivery, particularly with point-of-sale (PoS) devices and automated teller machines (ATMs) that frequently malfunction or run out of cash. A Facebook user, Mavuto Mwale, complained about the poor service at Standard Bank Malawi, stating, “I’ve been waiting in line for hours, and when I finally get to the counter, I’m told the system is down. It’s unacceptable.”

Bank branches often operate with limited staff, leading to extended wait times and rushed interactions that erode customer trust. Digital banking platforms, touted as solutions to overcrowding, frequently crash or fail during critical transactions, leaving customers in limbo. Emails and phone calls go unanswered for days or weeks, as evidenced in numerous complaints about National Bank’s handling of forex requests, where persistent follow-ups yield either silence or partial resolutions that fail to address the underlying issues. One customer reported making over a dozen calls to their bank’s customer service line over a three-week period without ever speaking to a representative, relying instead on automated messages promising callbacks that never materialized.

ATM networks present their own challenges. Customers report cards being swallowed by machines without explanation, money being debited from accounts without cash being dispensed, and prolonged periods where entire branches have no functioning ATMs. The resolution process for such issues can take weeks, during which customers are left without access to their own funds. By any reasonable measure, its a mad state of affairs.

A vicious cycle

Malawi’s banking woes cannot be divorced from the country’s broader economic struggles. As a resource-constrained economy dependent on foreign aid and agriculture, Malawi faces persistent vulnerabilities. Fluctuations in commodity prices, particularly tobacco, which accounts for a significant portion of export earnings – place continuous pressure on the kwacha and forex availability.

The International Monetary Fund’s 2025 Article IV mission emphasized the need for macroeconomic stabilization to create fiscal space for pro-poor spending, but high debt service bills and trade barriers continue to stifle progress. Foreign currency shortages are exacerbated by limited export diversification and a persistent trade deficit. When the national economy struggles to generate foreign exchange through exports, banks inevitably lack the forex reserves needed to serve their customers adequately.

Inflation, which has periodically spiked into double digits, further complicates banking operations. High inflation erodes savings, discourages deposits, and makes long-term financial planning nearly impossible for both institutions and individuals. Currency devaluations, while intended to address forex imbalances, often trigger price increases that outpace any benefits, creating a cycle of economic instability that banks struggle to navigate.

So what can be done?

Malawian banks aren’t inherently “bad,” but the combination of forex constraints, operational incompetence, infrastructural vulnerabilities, and subpar customer service has earned them a notorious reputation. Structural reforms could offer a path forward. Removing or relaxing forex surrender requirements – which mandate that exporters surrender a portion of foreign earnings to the central bank – could increase forex liquidity in the banking system, as suggested by the World Bank. Enhanced investment in digital infrastructure, including more reliable internet connectivity and robust payment systems, could reduce reliance on physical branches and improve transaction success rates.

But more importantly, staff training initiatives focused on customer service excellence and technical competence could address the human element of banking failures. Greater regulatory oversight and accountability mechanisms, including swifter resolution processes for customer complaints and penalties for systemic failures, might incentivize banks to prioritize service quality. And to not treat customers as a nuisance.

Similarly, customer complaints need to be addressed, as well as improved service delivery in terms of deliberate avenues which simplify the banking experience. For example, it’s unheard of that in 2025, customers should queue in a bank branch just to pick up a bank card – is it really that difficult o have a courier service that delivers cards to customers?

Until such reforms materialize, customers remain trapped navigating a system that feels designed to frustrate them rather than facilitate the movement of money. For a country striving to build economic resilience and attract investment, fixing its banking sector should be priority number one – lest more citizens and businesses turn to informal alternatives, further undermining the formal economy and reducing tax revenues that could fund the very improvements the system desperately needs.